Nobody else's system will make you profitable

Trading is a way of thinking, not a rule set you can copy.

This is Part 2 of a two-part series. If you haven’t read Part 1, start there.

The diagnosis is easy. The replacement is where most people get stuck.

You watch two traders take the same setup. Same chart, same trigger, same direction, taken within minutes of each other. One of them comes out with a nice profit. The other takes a meaningful loss on it.

They were looking at the same chart but ended up in completely different trades. They sized differently. One of them was already long something correlated and the other wasn’t. One got in early; the other chased it after it had already extended. They had stops in different places, different views on where the trade would be invalidated, and they didn’t even agree on what kind of market they were in.

By the end of the move, they’d survived completely different paths to where the trade was supposed to go.

The reason one of them ended up profitable and the other didn’t is the part of the job retail trading education doesn’t talk about. Most trading educators are teaching you what they themselves were taught and what they themselves seem to use. They run a policy too, but they don’t have language for it, so when they try to teach they teach the part they can name, which is the setup.

The rest happens on instinct and gets left out because it’s hard to point at something you can’t see clearly in yourself.

The setup therefore gets treated as the whole job. The layer underneath it, the size, the timing, the state, the path, what you’re already exposed to and what the trade does to your next decision, never gets named.

That’s where almost all the work lives, and almost all the difference between the traders who keep producing and the ones who don’t.

Last week I argued setups aren’t edges. The same pattern can be a clean trade in one state and a trap in another. A breakout, a failed low, a retest, a sweep, none of it means much until you know the state it’s happening inside.

This piece is about what happens once you accept that.

The harder question is what you do once the setup stops being the thing you’re deciding.

Nobody can hand you a profitable way to trade. Trading can be taught as a way of thinking, but not as a fixed rule set that transfers cleanly from one person to another.

The thing that makes money isn’t the setup itself but the judgment, built over years, to know when an action is worth taking in this state, under these constraints, with real risk on it. That judgment is hard to develop and it’s the only thing in this game that’s worth anything.

You still have to make decisions. Size, when to stand down, what the trade is worth, what it costs, what it does to your next decision, whether your read on the state is even close to right. None of those go away when the setup does.

The setup at least gave you something concrete to do with your hands. Without it, you’re left with the question itself:

Given the current state, what should I do?

The question sounds simple in the way that most important questions sound simple, which is to say it’s only simple before you try to answer it.

Most traders hear it and think the answer is selectivity. Take fewer trades, wait for cleaner setups, add another filter before clicking. But selectivity is still the old frame. It treats the setup as the thing being decided and just asks for a better-looking version of the same thing.

The real unit of decision is the state you’re in.

The market state. The account state. The volatility state. The liquidity state. Your own state. Your risk budget. Your attention. Your current exposure. What this trade does to the next decision.

Then the action: trade, wait, reduce, add, cut, hedge, or do nothing.

A checklist can help you remember what you planned for, but it isn’t the thing making the decision.

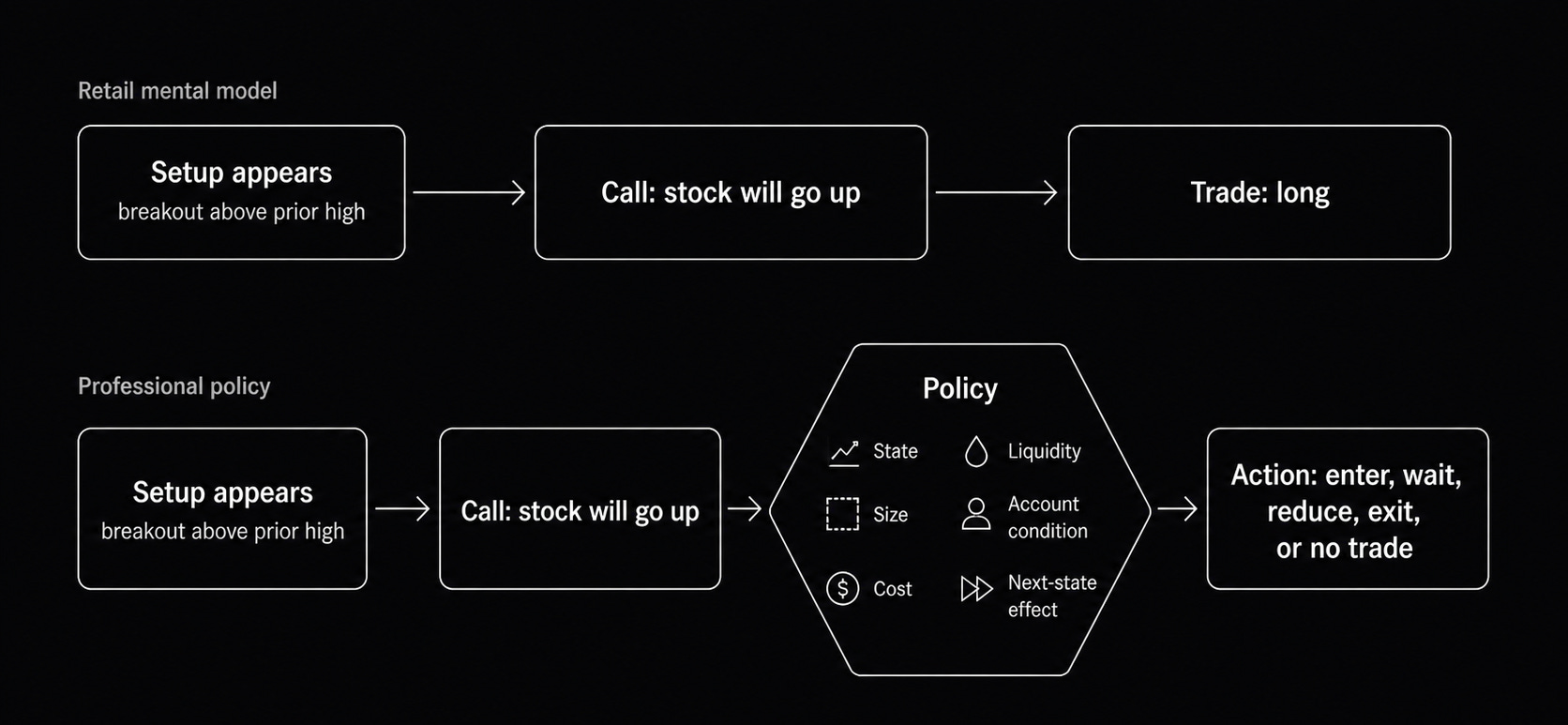

What you need is a policy.

A policy is your decision rule, the thing that tells you what to do given the state you’re in. The actions available to you are things like trading, waiting, reducing, adding, hedging, or sitting out, and the policy is what does the selecting.

Your policy isn’t automatically good; it’s just whatever rule you happen to be running right now. Some policies are better than others, and the optimal policy is the one that would maximize your risk-adjusted return over time if you ran it consistently.

Most traders aren’t running the optimal policy. They’re running whatever they’ve internalized so far, refined through trades and reviews and pain, and that’s what they’re slowly trying to improve.

Every trader is solving this problem, whether they know it or not. Quant or discretionary, the objective is the same: maximize expected value, minimize risk, stay in the game long enough for the math to compound.

What we call a policy is just the name for how you go about doing it.

No single rule covers every state. The clean textbook version of a setup calls for one action, the late or noisy version calls for another, the state where you’re already long something correlated calls for a third, and the policy is what tells you which fits which.

A setup tells you something might be there. The policy tells you what to do about it.

Most traders don’t have one. They have a setup, plus a rough sense of what to do when it looks clean. When it doesn’t look clean, they’re improvising, and they don’t always know they’re improvising.

The missing piece is the layer that would tell them which version of the trade they’re actually in.

Your policy isn’t fixed, and it can’t be. The optimal action depends on the state you’re in, and the state keeps changing, which means the optimal policy itself shifts over time.

You update your policy as you learn, based on what you’ve prepared for, what you’ve reviewed, what your account can take, and what the market is doing today. The work, in practical terms, is having a policy and running it and being honest with yourself about which of your trades came out of it.

Once the setup stops explaining the trade, what replaces it isn’t a better pattern but a better way of deciding what to do with whatever pattern shows up. That’s what sits underneath the rest of this piece: state, action, sizing, no-trade, discretion, review.

The first mistake is confusing the thing that gets your attention with the thing that makes the decision. That’s where the setup problem really begins.

A call isn’t a policy

The setup is what gets your attention. A breakout, a retest, a sweep, a failed low, a candle through a level. Whatever the pattern, it points your attention at something. The mistake is thinking the pointing already answered the next question.

It didn’t.

The setup alerted you. That’s all. From there you form a call: a view about what’s likely to happen next. The stock goes higher, the breakout fails, the low gets reclaimed. The call is your interpretation of what the setup might mean once you fold in everything else you know.

That’s how it gets taught. Pattern means action. Breakout means buy. Retest means enter. Sweep means fade. The trade feels justified the moment the pattern appears, because nobody ever taught the layer underneath.

But the pattern only flagged something for your attention. The call is a separate object. And even the call, once you have one, isn’t an instruction.

A call is information, not instruction. Same with a model, a level, an implied probability, or a volume read. None of it tells you what to do by itself.

The edge isn’t in the call. It’s in the policy that decides what, if anything, to do with it over a series of trades.

The setup pointed. The call interpreted. The trade is the action, and the action is what the policy chooses given the state.

When I’m reviewing trades with someone, this is the split I’m watching for. The call may have been right and the expression of it wrong.

You can be right about direction and still lose money. Size too large, ignore costs, execute poorly, exit emotionally, forget the correlation you already had on, or take a path you can’t psychologically survive. The call was right. The trade was still wrong.

You can have a weak call in a clean market, with low volatility, low cost, and deep liquidity, and still have something tradable. You can have a strong call in a thin, volatile market and still have no trade. The view didn’t disappear. The action changed because the state changed.

There are plenty of reasons to be directionally right and still have no trade. Upside too small. Stop too wide. Liquidity too thin. Volatility already exhausted. Trade already crowded. Exposure already booked somewhere else. Catalyst close enough to change the payoff before the position has time to work.

You think a stock will go up. It does. But you buy late, put the stop where every other late buyer put his, get shaken out by normal volatility, and watch the trade work without you. Good call, bad policy. That’s most retail traders who “know” which way the market is going and still bleed.

Or earnings. You’re right that the stock will miss and sell off. It does. You still lose because the puts were already priced for the move and the IV crush ate the payoff. Right direction, wrong expression.

“Being right” is a dangerous objective. It feels like the center of trading because that’s where the ego sits. The account doesn’t care whether you called it. The account cares about what you actually did. Size, cost, risk, timing, and the path you had to survive to collect.

A trade is the call expressed through size, timing, structure, cost, and risk. Sometimes the best expression is no trade.

The setup only points; the call only interprets; the policy is what decides.

No trade is part of the policy

Flat is part of the policy. So is waiting. So is reducing risk.

A sound policy often says “do nothing.”

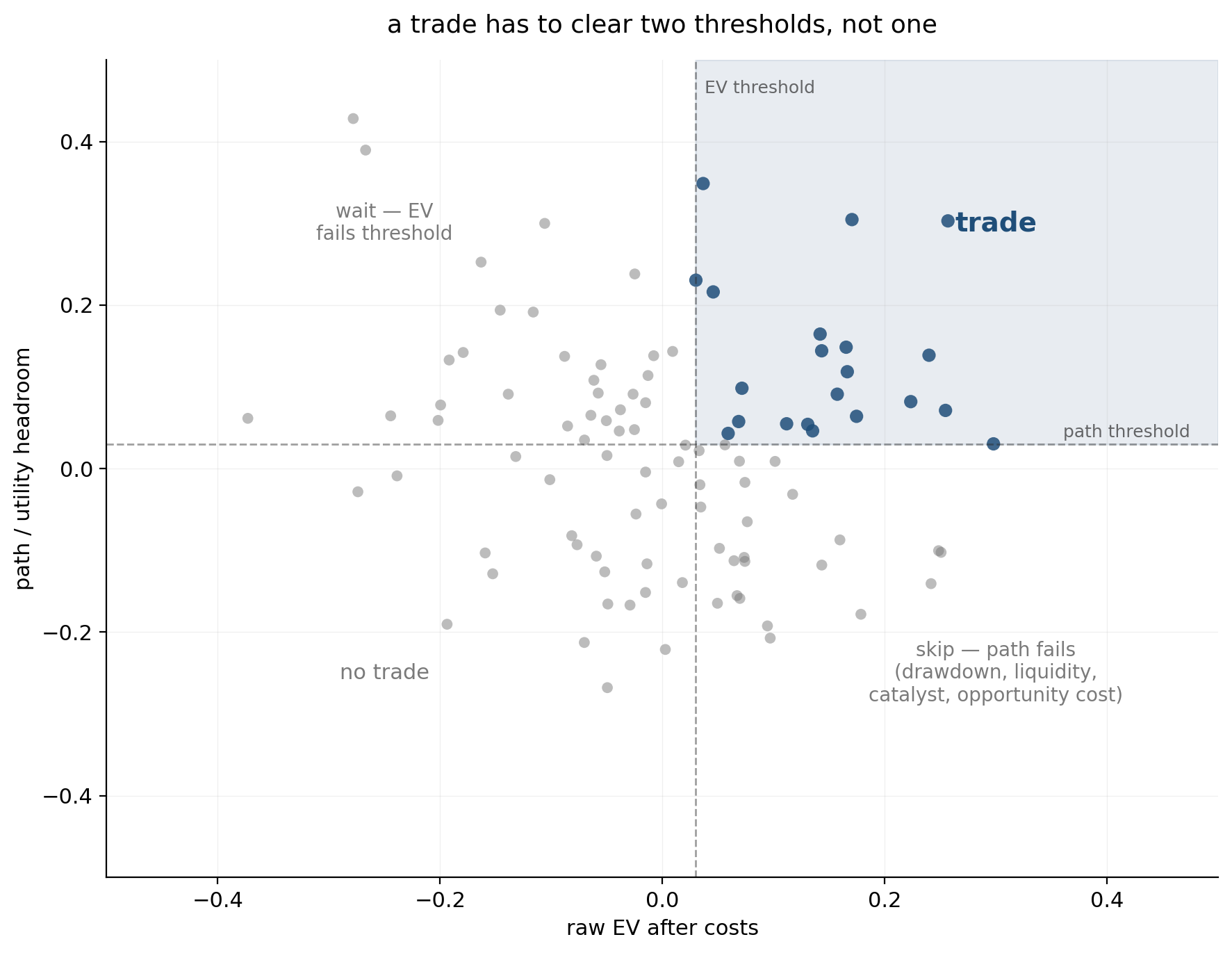

Sometimes the EV is there but the path is wrong. Drawdown is too deep. Liquidity isn’t there. The next catalyst is too close. Or the capital is worth more saved for the next state than risked here.

Most people treat no trade as a failure to find something. Often it’s the cleanest decision on the board.

Ask “Can I justify taking this?” and you can usually find a reason to participate. The candle closed. The level broke. The sweep happened. The setup gave you permission. But the market doesn’t pay you for finding a reason to click.

The trade has to be worth taking. Not whether it can win. Almost anything can win. The question is whether the action deserves the risk, given the rest of your exposure and the state you’re actually in.

Good traders often look less active than people expect. The amateur sees movement and feels opportunity. The professional sees movement and asks whether there is a clean action.

A market can move a lot and still offer no good trade. It can look obvious and still be untradeable because the risk-reward, timing, liquidity, or volatility is wrong.

In real life, that’s harder than it sounds. Sitting flat for three days while X is full of PnL screenshots from people taking the trades you decided not to take. The boredom and the low-grade anxiety, the voice telling you that you should be doing something because doing nothing feels like missing it.

That’s the real test: letting the policy keep saying no on day three when you haven’t taken a trade and your account is exactly where it was on Monday. The chart is moving. Your friends’ charts are moving. Your timeline is moving. Your account isn’t.

The people who blow up usually didn’t lack a setup. They couldn’t tolerate the absence of one. The boredom became unbearable, the FOMO got too strong, and the policy got overridden. Once that happens once, it happens easier the second time.

The reverse is also true. When the policy is sound, the sizing fits, and the market is actually offering opportunity, you should look forward to trading. Not anxious, not dreading the open, not white-knuckling every decision. Just willing to go to work because the work is worth doing.

Not because the next trade has to win. Because repeated exposure to the right states is the point.

If you dread the screen, the policy is wrong for you or the sizing is wrong. If you can’t stop clicking, same problem from the other direction. Calm willingness is the signal that the policy fits.

Cash isn’t dead capital. It’s the ammunition to act when the trade is worth taking.

That’s an easy sentence to write and a hard one to live by. Every move you don’t catch starts to feel like an accusation. The rally you missed becomes proof you should have been long. The selloff you watched becomes proof you should have shorted.

But movement and opportunity aren’t the same thing, and hindsight isn’t a decision process. A policy that can’t say no is just a participation machine.

Most opportunities don’t clear the bar. Doing nothing is a policy output.

When the policy maps the state to zero, nothing else needs deciding; when it says the trade is worth taking, the next question is how much of the account this state deserves.

Sizing is policy

Sizing exposes how well you understand the trade.

You can have a setup, a direction, and a reasonable read on what should happen next. Then the question becomes “how much,” and the whole thing gets exposed.

Long by itself doesn’t tell me enough. Long how much, from where, with what invalidation, in what volatility, with what execution method, with what account risk, and with what plan if the market confirms or does something ugly but not technically invalidating yet.

The action is the whole expression: direction, size, entry, stop, management, add logic, reduce logic, time stop, exit logic, and when to stop trading. That’s the trade. Not the entry.

The poker analogy works here. It isn’t enough to know that you probably have the better hand. You still have to know how much to bet, who you’re betting against, what future cards can change the state, whether your opponent understands the story, and whether the risk makes sense relative to your bankroll.

Trading is the same problem in different language. Size has to adjust for volatility, liquidity, drawdown, concentration, execution cost, and the consequence of being wrong. A high-conviction idea with bad sizing can still damage the account.

Bankroll management belongs inside the policy, not in a side note.

Sizing is one of the decisions, not a refinement you add later.

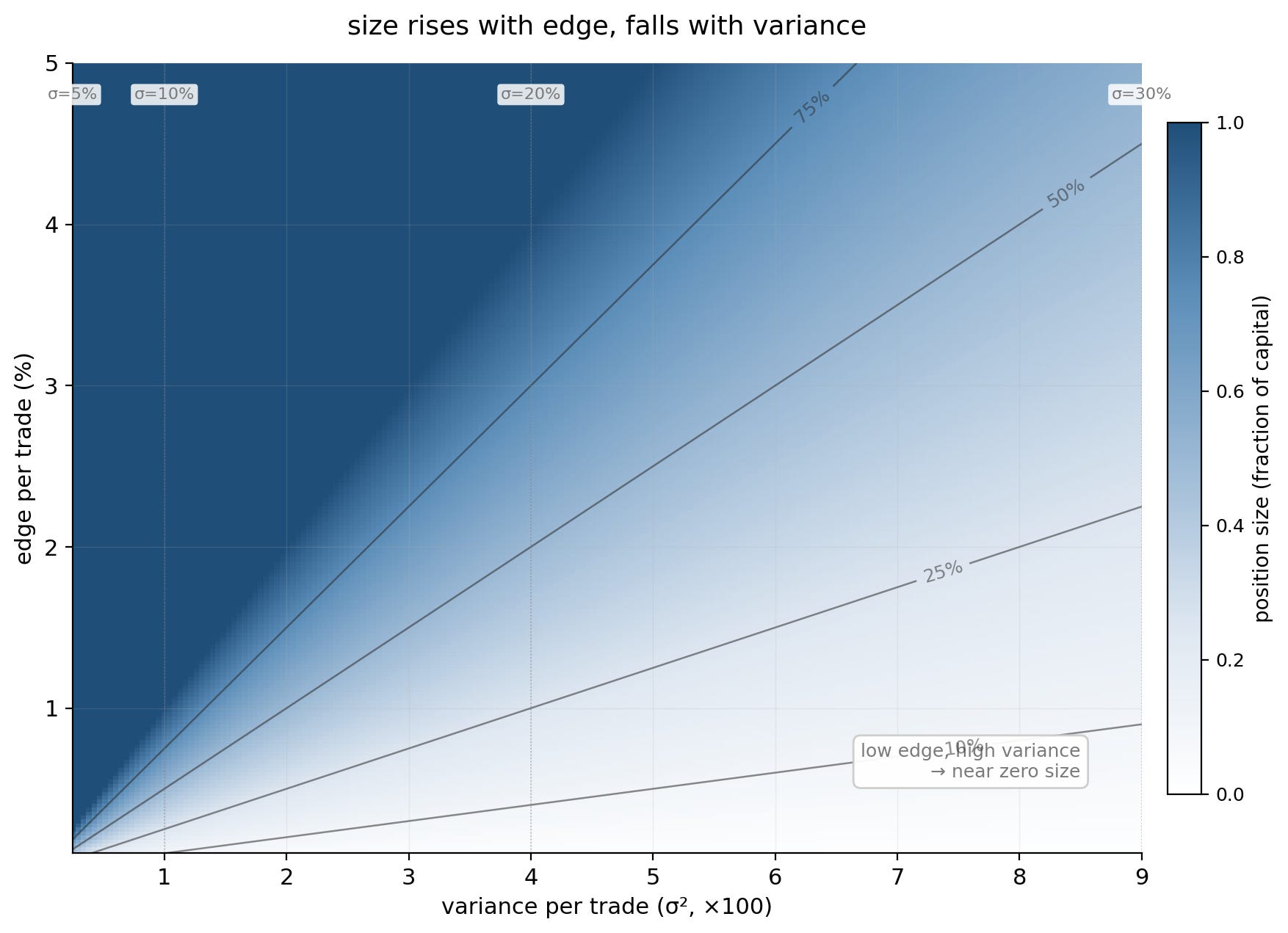

A simplified sizing intuition: size rises with edge and falls with variance, costs, correlation, and uncertainty in the estimate. That's the intuition, not the whole system.

If expected return rises, size may rise. Everything else cuts the other way. Higher vol pushes size down. Higher cost. Worse liquidity. Deeper drawdown. Higher correlation. Less confidence in the edge. Each one is a reason to size smaller.

Frequency is its own variance multiplier. Ten trades at the same per-trade size produce ten times the cumulative variance, not the same variance ten times. Size sets per-trade exposure. Frequency sets how many draws you stack.

The professional decision is more specific than “buy if expected return is positive.” It’s buy a specific size only if the expected return is high enough, the volatility is tolerable, the costs are low enough, the liquidity is there, the exposure fits, and the trade improves your overall risk profile instead of just making the position bigger.

Kelly sizing, fractional Kelly, vol targeting, portfolio construction. They all matter here. Not because you need to become a quant, but because edge and uncertainty have to be sized together.

Full Kelly is theoretically optimal for long-run log growth in a cleaner game than trading, one where the odds are known, the payoff distribution is stable, and you can estimate the edge with confidence. That isn’t the game we’re playing. The edge estimate is noisy, the regime can shift, liquidity can disappear, and the distribution can change right when you think you understand it. Nobody I work with uses full Kelly. They scale it down to half Kelly, quarter Kelly, volatility targeting, or some other constraint.

The point is the relationship between edge, uncertainty, and survival. If you lose all your money, you don’t get to keep learning. A drawdown that knocks you into emotional chaos impairs your future decisions even if you technically still have capital. An oversized trade that forces you to cut the next three good ones does more damage than the loss itself because it changes the path.

Every decision sets up the state you’ll be trading from next.

Take a marginal trade and lose, and the loss is only the obvious part. Now you’re in drawdown. You have less risk budget. You’re more emotional. When the next clean opportunity shows up, you’re not seeing it from the same place anymore.

The same thing happens in other ways. Capital tied up in a mediocre trade reduces flexibility. Bad liquidity can leave you stuck. And breaking process while still making money can be worse than losing, because now the market paid you to learn the wrong lesson. Confidence in the wrong behavior.

The better question isn’t only “can this trade make money?” It’s “what does this action do to my next state?”

Once size, execution, invalidation, and next-state cost are part of the action, discretion can’t mean feel. It has to mean picking the right branch of the policy while the state is still moving and you’re missing pieces of it.

Discretion is conditional logic

Discretion gets misunderstood. The word makes people think it means deciding from feel, and what often passes for discretion in practice is exactly that. You break your rules, move your stop, add because you’re annoyed, change your mind because the last candle scared you, and call the whole thing discretion.

That’s impulse with better branding.

Real discretion is something else, and it starts before the click.

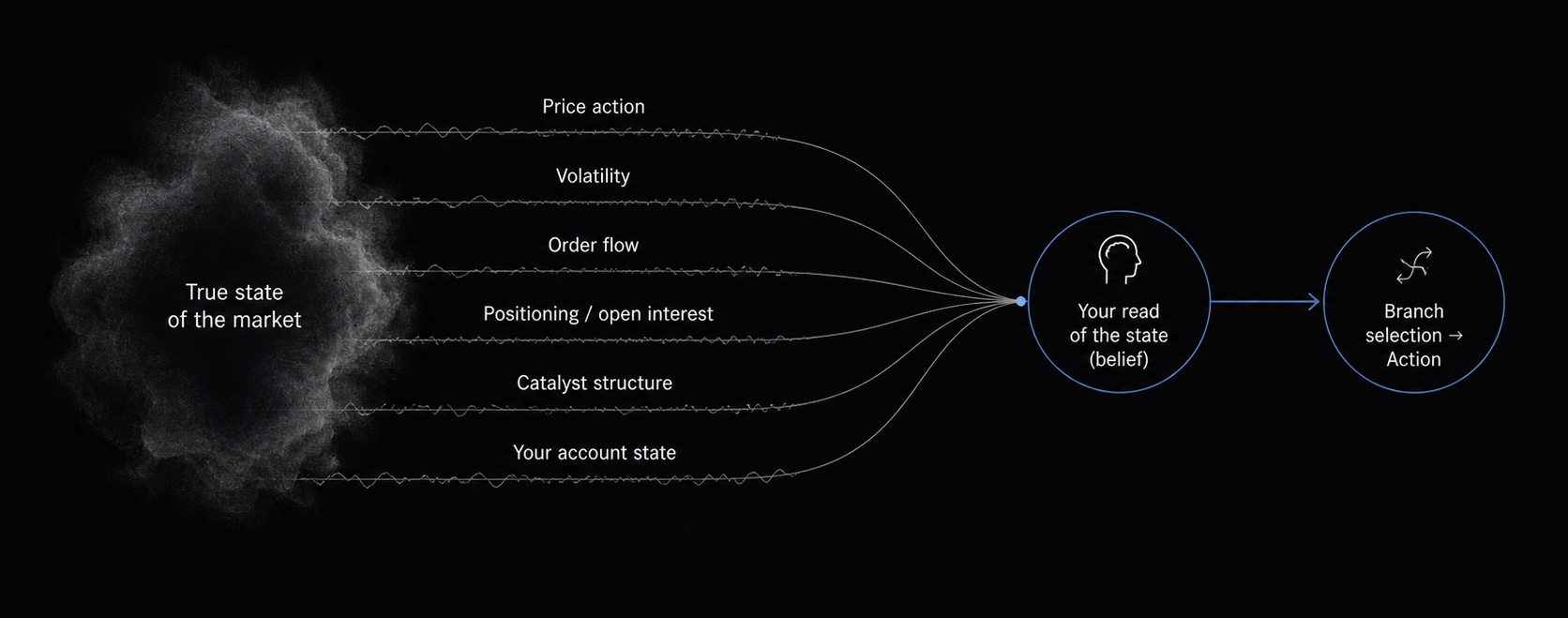

You never route from the true state. You route from your read of it. The read is built from noisy traces: price, volatility, flow, positioning, catalyst, your own account condition. That isn’t permission to improvise. It’s conditional logic.

It means the policy has branches. Rigid rules break because the state changes. A real policy changes its output when the state changes.

A breakout after compression, with participation expanding and room to reprice, can get you in. The same breakout after a stretched move into thin liquidity has you waiting, reducing, or staying out. Change the volatility or the exposure, and the branch changes. Move the catalyst too close, and it changes again.

The abuse starts when you take a rule you don’t want to follow, violate it in real time, and call the violation judgment. But judgment isn’t the feeling that arrives after risk is already on. Judgment is reading the state correctly before you act, then choosing the branch that fits.

Memorizing the action is easy compared with knowing which condition you’re actually in.

The traders I work with sometimes sound annoyingly vague to newer ones. They’ll say things like “I’d take that setup in this environment, but not here.” To someone looking for rules, it sounds evasive. To anyone who’s traded long enough, it’s the point. The setup is one variable. The policy decides whether that variable matters.

Regime is the state above the state. It decides which branches get paid and which ones get punished. A breakout policy that works in directional repricing gets chopped to pieces in balance. A fade built for a range gets destroyed in liquidation. The same tight stop that makes sense in calm volatility becomes self-sabotage when volatility expands.

That’s why “my setup stopped working” is often the wrong diagnosis. The setup didn’t disappear; the branch changed.

Markets don’t always remove the pattern when they remove the edge. The level is still visible, the sweep still happens, the breakout still triggers, the candle still closes. Everything looks close enough to tempt you back in. But the participants behind the move have changed, and so have the liquidity, volatility, and payoff. The reason the trade used to work may no longer be present.

That’s how traders end up worshipping dead setups. They aren’t imagining the pattern. The pattern is there. They’re confusing the shape with whatever made the shape matter in the first place.

Review has to separate a bad branch from a normal loss inside the distribution. Otherwise noisy feedback turns into corrupted policy.

The market can teach the wrong lesson

The market doesn’t give clean feedback. A good action can lose. A bad action can win. A good policy can look broken over a short sample while a bad one looks brilliant. A correct read can be early. A bad read can get bailed out by a headline. A sloppy trade can make money and teach you exactly the wrong lesson.

You want to update from the outcome because that feels natural. Green means good. Red means bad. Money came in, so the decision was right. Money went out, so the decision was wrong.

That’s too primitive. Green-trade-good and red-trade-bad isn’t learning. It’s mood tracking with charts attached.

The real question is whether the action made sense given what you could actually know at the time. Not after the candle closed, not after the breakout failed, not after you learned the news mattered or didn’t. At the decision point.

Did you read the state correctly? Did the setup actually express the imbalance you thought it did? Did the trade deserve the size? Was the execution good enough? Did you know where the idea was wrong? And when invalidation came, did you follow it or did you start negotiating?

What should the outcome teach you, if anything?

Sometimes the answer is “not much.” A trade can lose and still be good policy. The probabilistic side just played out the wrong way. A trade can win and still be bad policy that happened to get paid. The second one is more dangerous than people think. The market can pay you while making your policy worse.

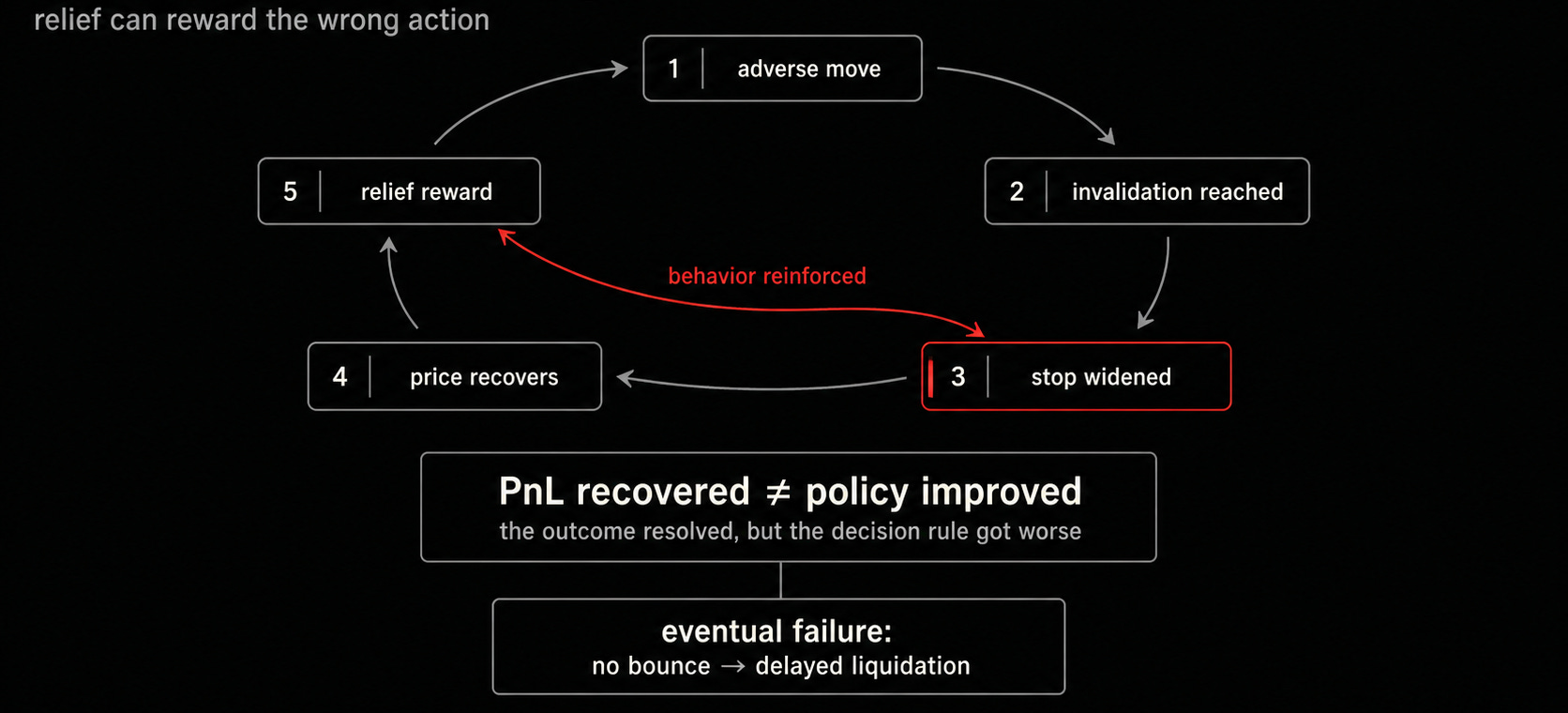

There’s a trap people miss. When a trade is deep in the red and you’re sitting there bracing for the real loss, you’re under pressure. When it comes back to breakeven, the relief can be enormous. Sometimes it feels better than a normal win because what disappeared wasn’t only the loss. It was the loss you had already started living through.

That relief is what keeps gamblers at the table. It feels like getting let off the hook. The brain remembers what behavior produced it. The behavior was widening the stop. So the brain learns to widen the stop.

The relief has nothing to do with whether the policy was right. The brain isn’t grading process. It’s responding to threat removal. A bad action that gets bailed out by a bounce can produce stronger reinforcement than a good action that simply pays.

You widen your stop because the level should hold. You add because price is better now. You defend the idea because taking the loss would make the mistake real. The market bounces, the trade comes back, the loser turns into a scratch, maybe even a winner.

What did you just learn?

If you aren’t careful, you learned that violating invalidation is judgment, that adding into adverse information is conviction, and that refusing to take the loss is patience.

False learning is reinforced by relief, not correctness. The PnL recovered. The policy degraded.

That’s how false learning enters the system. The reward feels good, so the update sticks. Then one day the market doesn’t come back, and that’s when you find out the setup wasn’t a strategy. It was a delayed liquidation.

When I’m reviewing trades, I want the review to live at the policy level. The point isn’t to explain the last outcome so you can feel better about it. The point is to improve your decision rule.

There are several things to separate when you review a trade. The outcome is what happened. The decision quality is whether the action made sense given the state you read. The execution quality is whether you implemented the decision properly. The policy update is what, if anything, should change as a result. Most reviews collapse all of that into a single verdict on the outcome, which is why most traders don’t actually learn from their trades.

Sometimes the policy was fine and the state read was wrong. Sometimes both were fine and the sample was just noise.

Without that separation, you become a slave to recent PnL. You win and assume you were right. You lose and assume you were wrong. You change rules after a tiny sample. You add filters after a painful loss, remove them after a missed winner, and become more reactive while thinking you’re becoming more experienced.

You don’t improve because you took another hundred trades and stared at more screenshots. You improve when you read the state more accurately, when you’re more honest about what you actually did, when you size better, when you execute cleaner, and when you stop being stupid about what your last few trades actually taught you.

That’s where teaching becomes useful. I can help sharpen variables, thresholds, sizing, and the review loop. I can’t hand anyone the optimal policy.

What can actually be taught

Markets aren’t pure noise, and neither is poker. If they were, skill wouldn’t persist. You wouldn’t see the same kinds of players and firms survive across cycles, and you wouldn’t see people keep getting paid in games designed to take their money.

Not every survivor has skill, and not every drawdown is noble. But if you watch long enough, the people who actually survive start to look different from the rest.

Stability isn’t proof of skill, but persistent stability across regimes is the closest signature we have.

The visible layer still matters. Experience matters. Knowledge matters too. You need language for recurring behavior, a way to organize price, and a way to talk about structure without starting from zero every time. Breakouts, sweeps, retests, order flow, volume profile, risk, sizing, probability, review, macro, options, execution, auction dynamics, liquidity, positioning, portfolio construction. All of it can be taught.

The failure is stopping there: names for patterns, no policy for when those names matter.

What can’t be honestly taught is a fixed rule set that prints money indefinitely. Trading isn’t a fixed-edge game. Edge changes, participants adapt, regimes shift. The same action that had positive EV in one state can turn negative in another.

Retail pattern transfer is not that game. Structural edges are something else, and Part 1 covered them.

I can help someone see more clearly. I can help them understand state, risk, sizing, review, and the difference between a trigger and a decision. What I can’t honestly promise is a fixed sequence of actions that will keep paying forever. That promise is the retail fantasy in a more expensive costume.

Useful education improves policy. A better policy can still be a losing policy, and losing slower is not the same as having edge. But policy improvement compounds. A card-counting policy in blackjack still contains basic strategy inside it. Counting adds a layer that changes bet size with the count, and sometimes changes the play itself. The old policy gets refined, not thrown out.

Teaching works because of that. I can’t hand someone the optimal policy. I can hand them pieces that move their current rule closer to it.

The useful questions are different from the ones most people are asking. What state does this setup require, and when does the same pattern stop mattering? Who’s likely on the other side, and is anyone forced to act? What does this action do to the next state?

That’s policy training.

A real playbook gives you more than the entry. It tells you what condition has to exist for the entry to matter. Who’s likely on the other side. Why their behavior should be predictable or forced. How much risk the state deserves. What would prove the idea wrong. And when the cleanest-looking version of the setup should still be left alone.

The cleanest trigger doesn’t always mark the best trade. The better trade is where the state, the action, the size, and the payoff all belong together.

That’s what you can actually learn from pros. Not a magic sequence of actions, not a holy grail strategy, and not “what the algorithms are doing” in some mystical retail sense. You learn what variables they pay attention to, how they define opportunity, how they manage risk and avoid bad states, how they size and review and think about costs, and how they keep one bad trade from damaging the next ten.

That actually takes pressure off. If you think professional trading is about finding the perfect setup, every loss feels like proof you still haven’t found it. Every missed move feels like evidence that someone else knows the secret. Every course, signal room, and screenshot thread becomes another possible doorway into the thing you’re missing.

If you understand trading as state-conditioned decision-making under uncertainty, the task becomes less mystical. Still hard. Less fake. You’re no longer hunting for the one pattern that removes uncertainty. You’re building a better policy for acting while uncertainty remains.

The system gets replaced by policy, not by a better pattern. Judgment becomes trained. The setup can still matter, the level can still matter, the trigger can still matter, but none of them get to make the decision for you.

The beginner wants to know what price will do. The professional doesn’t get that luxury. He has to act well without it.

More of this in book form: The Art & Business of Professional Trading

Further reading

If you want the deeper technical analysis argument, read Does technical analysis “work”?.

If you want the edge-decay version, read Edge isn’t yours.

If the review / psychology section hit closest to home, read Why working on your trading psychology is making you worse.

Overall - lovely read, both articles - though question - how does one know the probability in that particular state when the are SO MANY variables? Feels literally impossible to backtest or even properly journal in a meaningful way.

Let’s go man! Sinking into this one later today!