A setup is not an edge

Most retail traders are taught to memorize patterns. Professional trading starts when you realize the setup is only a trigger inside a state.

This is Part 1 of a two-part series on what professional trading actually is and why most of what gets sold to retail traders misidentifies the job. Part 1 sets up the problem — why setups don’t work the way you’ve been told. Part 2 is the harder half: what actually replaces the system once you stop chasing it. Read it here.

Quick note before we start. My book, The Art & Business of Professional Trading, is now out from Wiley.

It expands on the same idea this essay is built around. Trading is not a collection of setups. It is a professional decision-making business.

You can find it on Amazon, your local Amazon store, or wherever you usually buy books.

You can get it here.

Now, on to the article.

If you’re looking for the system that will make you consistently profitable, you’re operating inside the retail fantasy of trading.

The fantasy is that trading can be learned as a system: find the setup, memorize the rules, wait for the signal, place the stop here, take profit there, then repeat the process every morning until you’ve built a second income and a way out of your 9-to-5.

That is not how the job works.

Open YouTube and search “trading strategies.” The fantasy is being sold in every variation.

The only trading strategy you’ll ever need. The setup that prints money. The impossible-to-lose indicator. The boring strategy that makes $44,000 a month.

Different packaging. Same promise. Learn this thing and start printing cash.

That’s where the grift lives.

Not everyone selling this stuff is consciously lying. Some are. Plenty know exactly what they’re doing. But a lot of them are just downstream of the same false model.

Some have never done the job at a professional level, so they reduce trading to the only layer they know how to package: setups, screenshots, entry rules, trade recaps, and clean before-and-after examples.

Others aren’t necessarily scammers. They’re survivors. They found a path that worked for a while, got paid by a particular market environment and then confused the result with understanding.

Maybe the setup really did work for them. Maybe they were in the right product, at the right time, with the right volatility, in the right regime, before the edge got crowded or decayed. Maybe they were good. Maybe they were lucky. Usually it’s some combination of both.

But once the PnL shows up, the story gets cleaned up. The messy path becomes “my system,” the favorable regime becomes “my edge,” and the survivor becomes the teacher.

Now a trader who got paid in one environment starts selling the thing that worked for him like a portable rulebook anyone can take into any market and run.

That’s the problem.

A system is easier to market than judgment. A setup is easier to sell than state-conditioned decision-making.

A rulebook is easier to sell than the ugly work of learning when a rule applies, when it doesn’t and when following it is exactly what gets you run over.

So they sell the system as if it were the job.

It isn’t.

And this is where the argument usually gets misread.

The problem isn’t technical analysis. The problem is pretending technical analysis has already made the decision.

A breakout can matter. So can a sweep or a pullback. Technical analysis can help you organize what you're seeing, where attention is clustering, where stops might be sitting, where liquidity might be vulnerable and where other participants might be forced to respond.

I wrote about this in more detail in Does technical analysis 'work'?, where I argued that TA can help organize market behavior, but becomes dangerous when traders treat the map as the decision.

What it doesn’t do is make the decision for you.

A chart pattern with an entry rule doesn’t tell you what state the market is in, whether the trade is worth taking, how much risk it deserves, what liquidity it requires, what costs it has to overcome, what account condition it fits or when the exact same pattern should be left alone.

Without those answers, you don’t have a strategy. You have a thing to click when the chart looks familiar.

That model is bullshit because it confuses a visual trigger for a complete decision. I’ve watched too many traders get trapped there.

Here’s why.

Trading is a decision game

Trading isn’t a puzzle that resolves once you collect the final piece. It’s a repeated decision game under uncertainty.

If that sounds less exciting than “learn one setup and quit your job,” good.

It should.

The real job is less marketable than the fantasy.

You’re making decisions with incomplete information, against other participants, inside an environment that changes while you’re trying to understand it. The thing you’re studying is moving. The people inside it are adapting. The feedback is dirty. A good decision can lose. A terrible decision can get paid. The same action can be brilliant in one condition and stupid in another.

When I’m reviewing a trade, this is the question I care about.

Not “what setup is this?”

But “given this state, what action is worth taking?”

The symbols matter less than the plain English.

A policy is just a rule for action:

Given this state, choose this action.

That is the job compressed into one line.

When I work with traders, this is usually the first major shift I’m trying to make.

Stop asking whether the setup appeared. Start asking whether the action made sense from the state.

The action might be to enter long, enter short, do nothing, reduce size, add, exit, hedge, wait, scratch, lower exposure, stop trading for the day, change markets, switch strategy, or leave the whole thing alone because the state is not worth risking capital in.

That is already a completely different model than the retail version, which usually reduces the job to:

“When do I buy?”

Professional trading asks something harder:

“Given this exact state of the world, what action has the highest expected utility after costs, risk, liquidity, sizing, drawdown, constraints, and future opportunity are considered?”

That is the real decision.

Not the setup.

The action from the state.

That mental model is almost never taught to retail traders. Professional trading isn’t the search for a magic pattern. It’s the process of making better state-conditioned decisions under uncertainty, with risk, sizing, liquidity, cost, drawdown, objective, and future opportunity all included in the decision.

That is where the retail model breaks.

The setup was never the thing. You start asking what the setup means inside the current state, whether the action attached to it has positive expected value, whether the risk is worth taking, whether the size is survivable, and what the trade does to your next decision.

That’s the job beneath the chart.

It’s more honest and more difficult than the fantasy. It’s also more learnable.

Start with the decision problem

Start with what’s actually happening when a trader makes a decision. The first mistake I see over and over is treating trading like a prediction problem.

Will this stock go up? Is this bullish? Is this bearish? Will the breakout work? Will the level hold?

Those questions aren’t entirely useless but they’re incomplete.

A trader isn’t paid for predicting correctly in some clean abstract sense. He’s paid for choosing the right action under uncertainty, after risk, cost, liquidity, sizing, execution, drawdown, constraints, and future opportunity are accounted for.

A stock can be likely to go up and still be a bad trade. The edge might be too small, the stop too wide, the spread ugly, the options overpriced. You might already have the same exposure somewhere else, or a catalyst ten minutes away. You might be in drawdown, one bad trade away from turning a normal loss into emotional damage.

The question isn’t “what do I think will happen?” The question is “given the current state, what should I do?”

That’s the whole game hiding in one sentence.

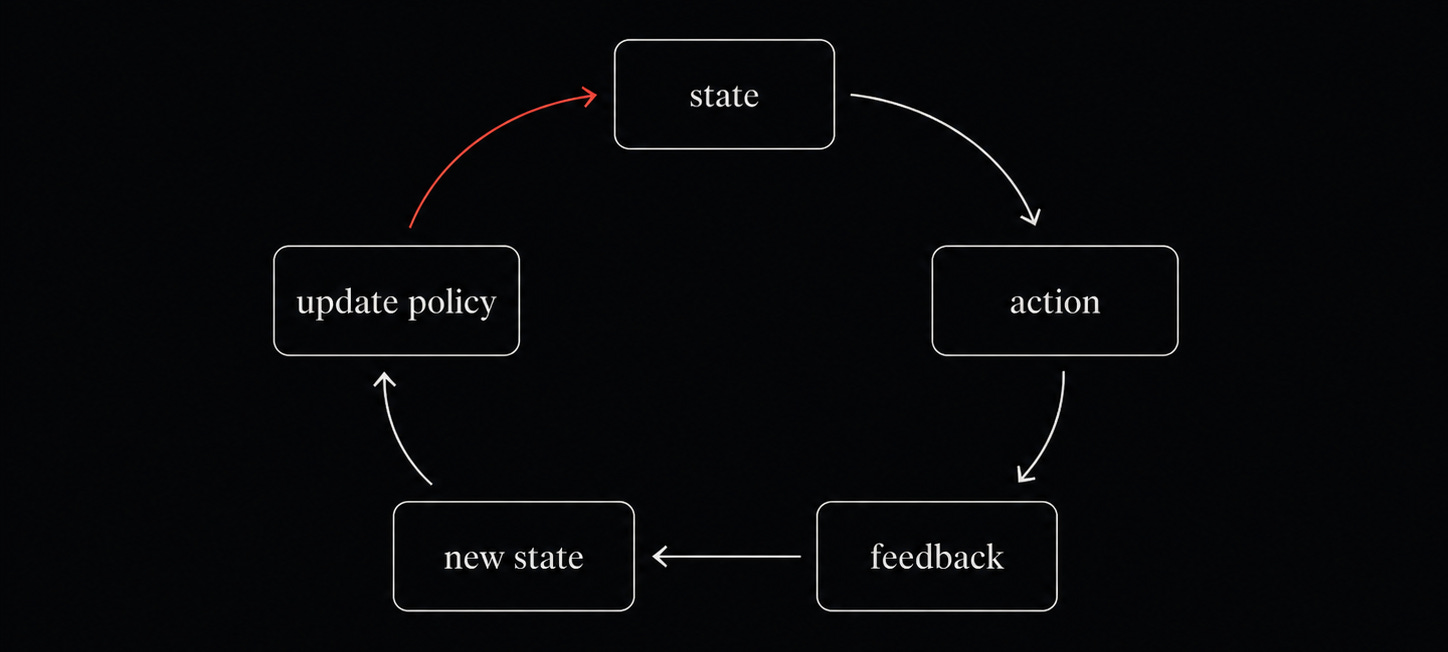

At each moment, the trader is inside a loop.

Formally, the loop looks like this:

The trader observes a state, chooses an action, receives feedback, and lands in a new state.

But in trading, the feedback is dirty.

The current state leads to an action. The action produces feedback. The feedback leaves you in a new state. Then you carry whatever you learned, or whatever you falsely learned, into the next decision.

In plain English:

State — What condition am I actually in?

Action — What can I do from here?

Reward — What happened after I acted?

Next state — What did this action do to my account, exposure, risk budget, emotional state, and opportunity set?

That loop matters more than any setup.

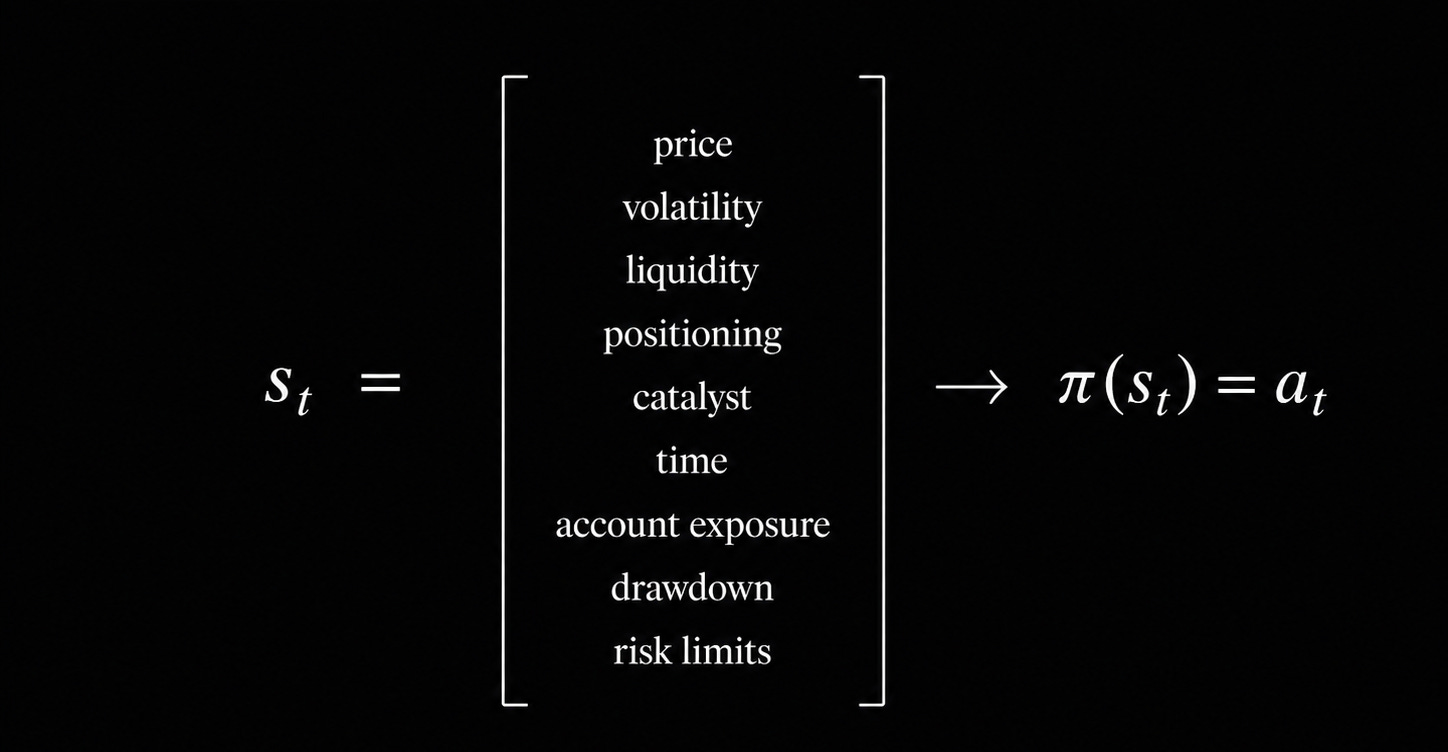

The state isn’t just price. It includes volatility, liquidity, trend, time of day, catalyst structure, correlations, order flow, current positions, drawdown, risk limits, margin usage, spread, regime, and whether the market is likely to punish or reward urgency.

A trading state is not one variable. It is a bundle of conditions.

Traders usually collapse all of that into one visible thing:

That’s the error.

The chart pattern may be part of the state, but it is not the whole state. When a trader treats the visible setup as if it contains the entire decision, he is compressing a high-dimensional problem into a screenshot.

It also includes you.

If you slept four hours, you’re down on the year, and you’re still annoyed from the last scratch, that’s part of the state. The DOM may look identical to yesterday. But you don’t. A professional policy has to account for that. A bad one pretends the trader is a constant.

The same setup taken by the same person in two different mental conditions isn’t the same trade.

One version is calm, sized normally, willing to wait. The other version pushes the marginal trade because doing nothing feels intolerable, sizes up because he’s down on the day then starts adjusting his stop because taking the loss would confirm the morning isn’t working.

Same chart, different operator, different distribution.

The action space is larger than most traders realize.

The action is not just buy or sell. It can be enter, exit, hold, reduce, add, hedge, wait, scratch, lower size, change markets, stop trading for the day, or do nothing.

And even that is too simple, because a real trading action includes size, entry, stop, invalidation, time horizon, exit logic, and management rules.

That’s why “I called the direction” means very little.

Direction is only one component of the action. A trader can get direction right and still have the wrong size, wrong location, wrong stop, wrong time horizon, wrong liquidity, wrong management, and wrong risk profile.

That means the feedback is more complicated than green equals good and red equals bad.

This is where I see traders get wrecked. They treat PnL as a clean grade.

But professional feedback is broader than the result of the trade. It includes what the action did to the trader’s next state: capital, drawdown, exposure, risk budget, emotional condition and future opportunity.

I don’t care that a trade made money if it taught you to violate your stop. That’s not clean reward.

A trade that loses money but follows a good policy in a noisy environment isn’t automatically a mistake. A trade that ties up capital, expands correlation, worsens your drawdown, and makes you miss the next clean opportunity may be a bad action even if the entry signal was “right.”

The trade isn’t isolated. It changes the state you inherit next.

You aren’t taking one trade in a vacuum. You’re walking a path. Every action changes the account, the trader, the risk budget, the future opportunity set, and the next decision.

A trade is not just a one period bet.

It changes the next state.

The value of an action is not only the immediate result. It is also what the action does to the future.

This is extremely relevant to trading.

A marginal trade may not look dangerous by itself. But if it puts you near your daily loss limit, damages your patience, consumes your attention, increases correlation or causes you to miss the next clean opportunity, the true cost is larger than the trade’s PnL.

Professional traders think in paths.

Amateurs think in isolated trades.

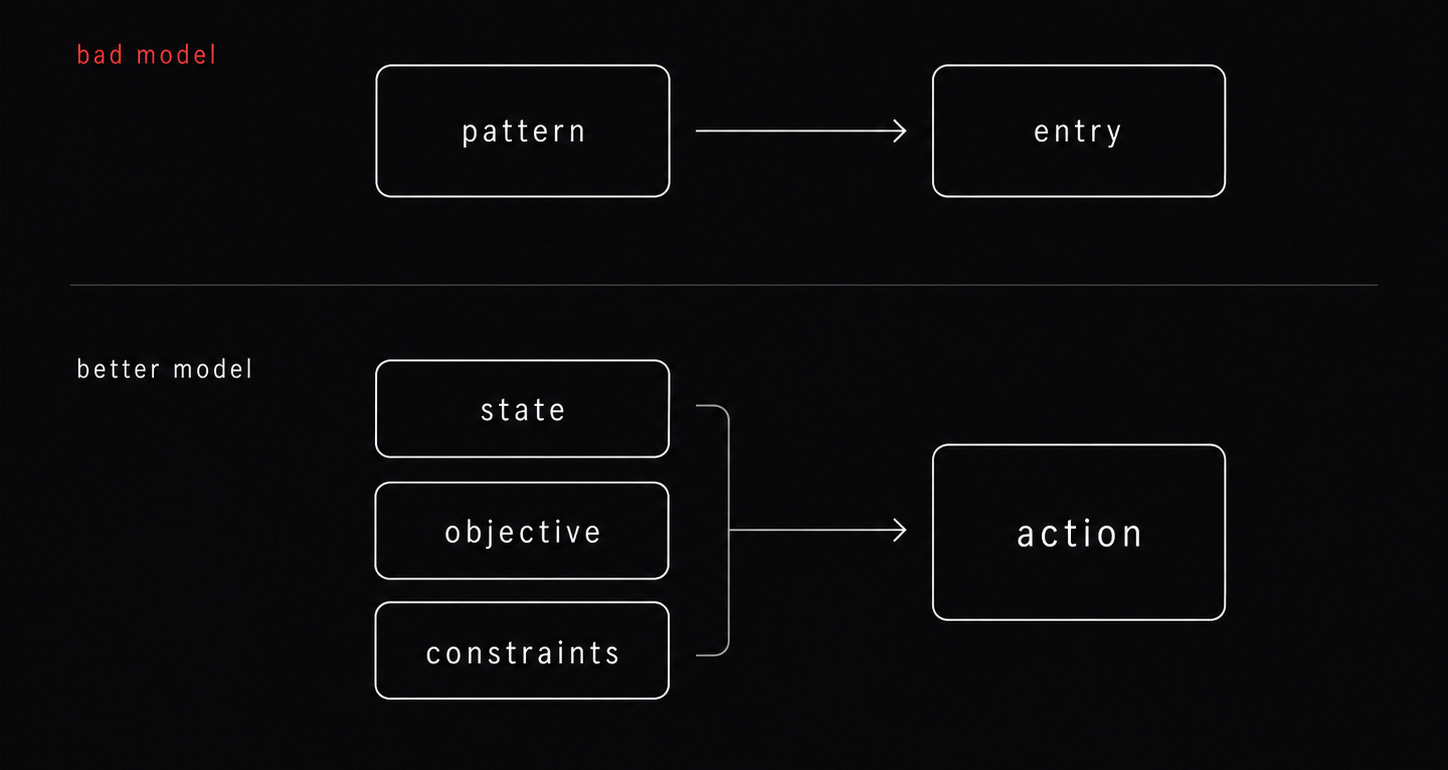

What a policy actually is

Once you start with the decision problem, you need a word for the thing underneath the trade. Not the setup, not the forecast, not the entry. The thing that turns a condition into behavior.

That’s the policy.

A policy is the rule, process, or internal operating system that maps a state to an action. Given this kind of condition, the trader does this. Given another kind of condition, he does something else.

It doesn’t have to be academic. Every trader already has one. Most just don’t know it.

A struggling trader may have a policy that looks like this, even if he has never written it down:

When price moves without me, chase. When I’m down on the day, increase size. When my stop is about to hit, widen it. When a trade immediately goes green, take profit because I don’t want to feel it come back. When I miss the clean trade, find a worse version and pretend it’s the same thing.

None of that is written down.

It’s still a policy.

The trader enters a condition, and his system outputs behavior.

Professional trading is the attempt to make that mapping better.

Reinforcement learning gives us useful language for this, but the idea is simple.

A policy, usually written as π, maps state to action.

Given this state, choose this action.

The ideal version is π*, pronounced pi star.

Again, the notation is just shorthand. Pi-star means the best possible version of the policy.

It isn’t a crystal ball and it isn’t the action that magically knows the next candle. It’s the decision rule that would choose the best probability-weighted action from every state, given the objective, the constraints and the distribution of possible outcomes.

Your job, and mine, is to get as close as possible to that kind of action selection in a market that never gives us the full picture.

That distinction matters because the optimal action can still lose.

If the best available action carries a 60% chance of a +1R win and 40% chance of a -1R loss, π* still takes the trade. If this instance falls into the 40%, the decision wasn't wrong. The outcome was bad.

In trading, π* is the theoretical ideal.

It is the perfect state-to-action policy we would have if we could evaluate every relevant condition: volatility, liquidity, regime, catalyst structure, positioning, account state, risk limits, costs, constraints and future opportunity.

It would not know the future.

It would know the best action to take under the full range of possible futures.

Of course, no trader actually has that.

Markets are noisy, adaptive, partially observable, and always changing. We never see the full state. We infer it from traces. Regimes shift. Liquidity disappears. Edges decay. The thing that worked for six months can stop working right when the trader has the most confidence in it.

Markets are also adversarial.

The same prices you’re trying to read are being read by people whose job is to take advantage of how other traders read them. The participants on the other side are running their own policies, and some of those policies are designed to exploit predictable behavior like yours.

When too many traders run the same setup the same way, the market starts paying the people who fade them instead. The level holds, then it doesn’t. The breakout works, then it traps. The thing that fed you for two years can stop working not because you forgot how to execute it, but because the trade got crowded, the payoff changed, and the rest of the room started seeing the same thing.

That is why no trader gets to operate from certainty.

The professional trader is not executing π*.

He is improving π̂, pronounced pi hat.

π̂ is the policy you actually have. I have one. You have one. Every trader has one, whether it’s written down or not. It’s your current approximation. The rule for action you know how to run right now, built from evidence, experience, models, constraints, mistakes, and scars.

That approximation may be good, bad, incomplete, fragile, regime-dependent, overfit, under-tested, emotionally corrupted, or simply not mature yet.

Not truth, not certainty, not the perfect answer. Just your best current approximation.

Professional development is the attempt to improve that approximation.

Of course, we never reach the perfect policy. The point is to move the approximation in the right direction through better state recognition, better action selection, better sizing and cleaner review.

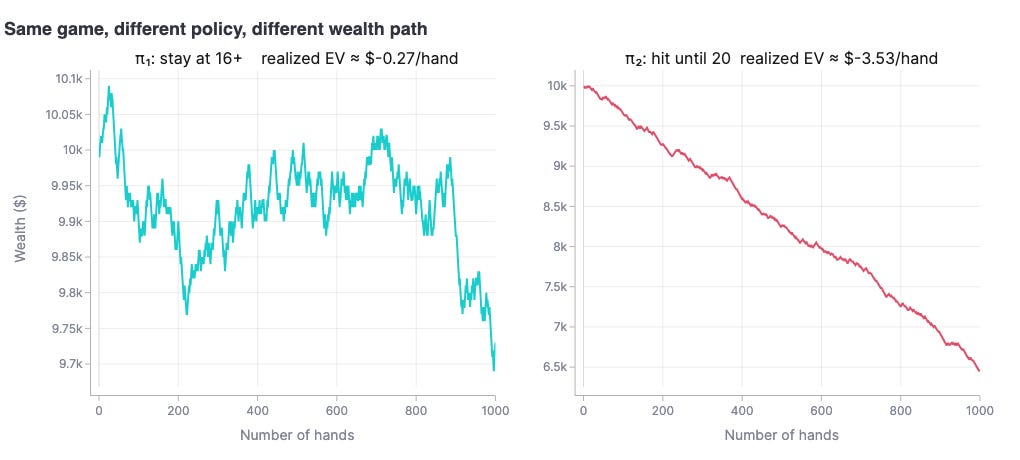

I use blackjack here only as a toy example. Markets are much more complex but the policy point is obvious.

Same game. Same environment. Two different action policies. The wealth paths diverge because the decision rule changed.

That’s the point of policy. It is not the hand, card, setup or signal alone that determines the path. It is the action rule applied to the state.

Same game, same environment, two different action policies. The wealth paths diverge because the decision rule changed. This is the point of policy: it’s not the hand, card, setup, or signal alone that determines the path. It’s the action rule applied to the state.There’s no universal optimal policy

This is another reason fixed system education is nonsense.

There’s no universal π* because there’s no universal objective. The optimal policy depends on what the trader is trying to do.

Different participants can look at the exact same price and take opposite actions, both correct.

A market maker is fading a move to earn the spread, focused on keeping inventory flat. A trend follower is buying that same price because he’s trying to catch a regime shift and a few ticks of heat don’t matter to him. A stat arb trader isn't even taking a directional view. He's running a relative bet against another instrument. An options trader may not care about direction at all and instead be trading implied versus realized volatility, or skew, or gamma. An execution trader isn’t expressing an opinion. He’s just trying to move size without leaving a footprint.

Same market, different objectives, different policies.

It’s like asking for the optimal vehicle. Optimal for what? Racing? Moving furniture? Crossing the desert? Parking in Manhattan? Driving on snow?

The objective defines the policy.

Which is why “just follow this system” is such a childish framing.

A rule is not optimal in the abstract. It can only be evaluated against an objective, a state space, an action space, a cost structure and a reward function.

Retail education usually skips that part because the real version is harder to sell.

“Buy this setup” is clean.

“Define the objective, identify the state, choose from a constrained action set, account for cost and risk, then update the policy from noisy feedback” doesn’t fit into a thumbnail.

But that’s much closer to what the job actually is.

Almost. Fixed rules do work in a few corners of the market: latency arbitrage, certain market making books in less competitive venues, regulatory and capital structure arbitrage. The edge there is structural, not predictive. It comes from being closer to the exchange, holding a license nobody else can get, or sitting in a balance sheet position the rest of the market can’t take. Those traders run the same playbook on Tuesday that they ran on Monday because the source of their edge isn’t going anywhere.

Retail isn’t doing any of that. Retail is trying to predict, and prediction in a market full of adaptive participants doesn’t sit still long enough to be turned into a fixed system.

A setup is a trigger inside a state

Once we understand policy, the setup gets put back where it belongs.

It isn’t useless. It’s just not the edge by itself.

A breakout, pullback, sweep, retest, imbalance, failed auction, opening range breakout, VWAP reclaim. Whatever name the tutorial slaps on it, none of these are universal objects. They don't behave like machine parts you can drop into the market and expect to work the same way every time.

They’re visible events.

They may point to something real. A breakout can reveal initiative buying, a sweep can reveal trapped positioning, a pullback can offer better location, and order flow can show pressure, absorption, urgency, or exhaustion.

But the event itself isn’t the edge.

The edge depends on the state in which the event appears.

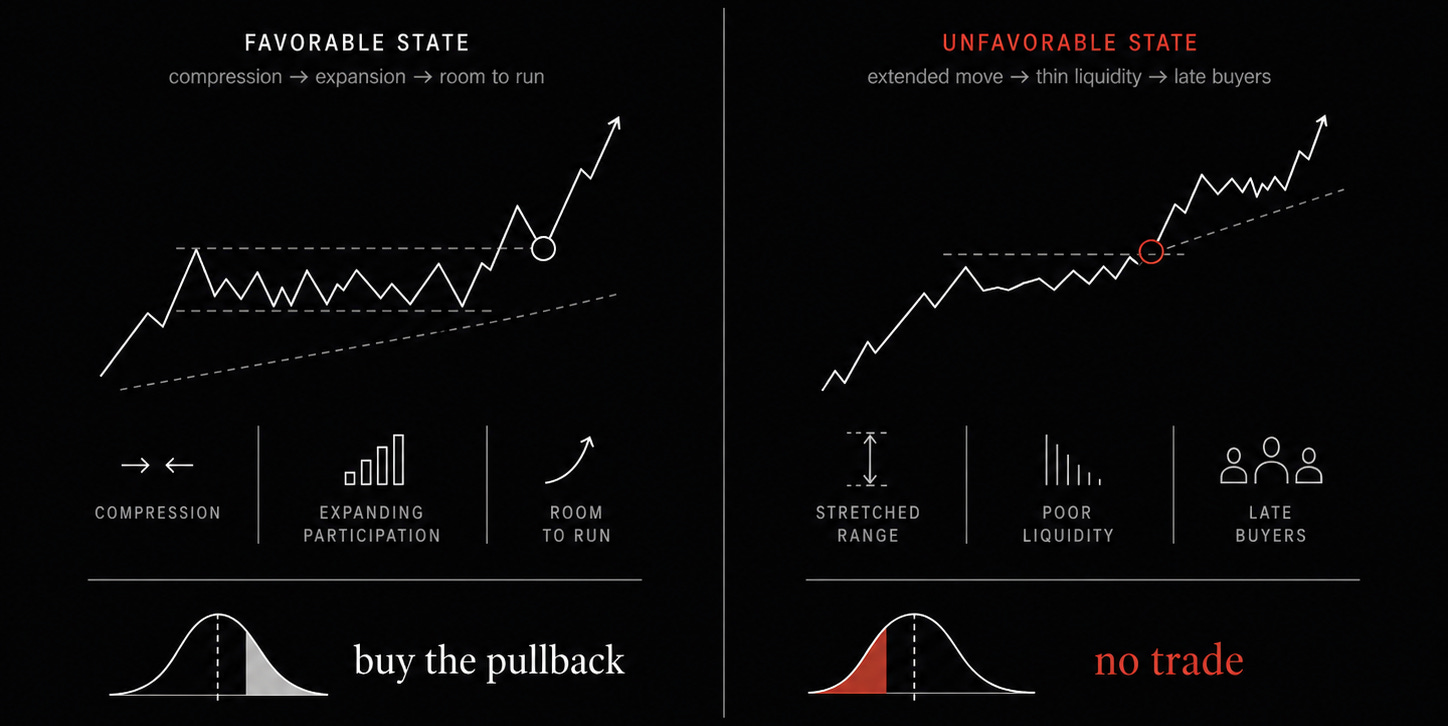

A football play is a useful analogy. “Run the ball up the middle” isn’t good or bad by itself. It depends on the defensive front, down and distance, field position, clock, score, weather, personnel, fatigue, and what the other side expects. The play only makes sense inside the state of the game.

Trading is the same.

“Buy the breakout” isn’t good or bad by itself.

Buy which breakout?

The one after three days of compression, with volatility expanding, participation coming in, shorts offsides, and room for repricing?

Or the one after price has already moved one and a half times the daily range into dead midday liquidity, where late buyers are finally chasing the thing after most of the opportunity is already gone?

Same label, different state, different distribution, different trade.

The sequence is:

The setup is only one part of the state. The state changes the distribution. The distribution determines expectancy.

Retail education usually stops at the first link.

Professional trading starts asking about the rest.

A setup is closer to a symptom than a diagnosis. A fever is real and measurable and it matters, but no serious doctor treats the number on the thermometer as the whole diagnosis.

One patient has a mild virus. Another has sepsis. Another is reacting to medication. Another just finished running in the sun.

Same symptom, different condition, different action.

Most traders miss this piece. They ask whether the setup works, as if the setup owns its own expectancy, when it doesn’t. The setup is a trigger inside a condition. The condition determines what kind of outcome distribution you’re drawing from.

State is just a plain word for the full condition you are acting from.

Not just price.

Volatility, liquidity, positioning, catalyst, time of day, prior movement, regime, correlations, event risk, execution cost, current exposure, drawdown, risk limits, margin usage, attention, fatigue, and whether someone on the other side is forced to act.

The setup is only one input. The policy acts on the full state.

And even that’s still incomplete, because in markets you rarely observe the true state.

You don't see the real intentions of other traders or all the hidden liquidity. You don't know the next piece of news.

You don't know whether the move is informed or random, whether a signal has decayed, or whether a regime has changed. By the time you do, the damage is already done.

Trading isn’t only state-dependent, it’s partially observable. You aren’t acting on the true market state. You’re acting on your belief about it.

Which is closer to poker than roulette. You don’t know your opponent’s cards. You observe the bet sizing, timing, position, stack depth, prior behavior, and texture of the hand. Then you act based on a probability distribution over what might be true.

Markets work the same way.

The market doesn’t reveal the truth. It gives you traces.

A pullback in a strong directional auction isn’t the same thing as a pullback in balance. In one state, buyers are absorbing supply and the pullback gives you a cleaner location to express a view. In the other, price is just rotating through inventory and the same pullback may have no informational value at all.

The same is true for sweeps. During real volatility expansion, a liquidity sweep may reveal forced selling, trapped traders, or failed continuation. In thin conditions, it may just be price passing through an obvious level because nobody meaningful was there.

Or take a failed breakout. After a major catalyst, it may tell you the market rejected new information. On a random Tuesday afternoon, it may tell you nothing beyond the fact that a level was obvious.

Retail language gives those events the same name.

Professional thinking doesn’t.

This is why technical analysis taught without state becomes fragile. It names shapes, but it doesn’t define the condition in which those shapes have edge.

It gives the trader a visual category, not a decision category.

A trader who learns visual categories can say:

“This is a breakout.”

A trader who learns decision categories can say:

“This is a breakout after compression, with expanding volatility, strong participation, clean structure, and room to run, so buying the first pullback may have positive expectancy.”

Or he can say:

“This is a breakout after exhaustion, into poor liquidity, with no room left in the payoff, so the correct action is no trade.”

The word breakout appears in both sentences.

The trade doesn’t.

Price doesn’t move because a pattern completed. Price moves because someone has to transact. The transactor might be late, trapped, hedging, or puking risk. He might be providing liquidity because his mandate says he has to, not because he thinks the trade is good. Either way, he’s acting under constraints that may have nothing to do with the pattern you’re staring at.

The pattern may help you locate that behavior, but it isn’t the behavior itself.

A breakout isn’t demand. It may reveal demand.

A sweep isn’t trapped positioning. It may reveal trapped positioning.

A pullback isn’t opportunity. It may create opportunity if the surrounding state makes the next action worth taking.

Setup education skips this part because the visible layer is easier to package. You can put a setup in a screenshot, memorize it, and hand it to a student. State has to be explained and re-interpreted on the fly. A setup gives the student something to copy. A policy forces him to think conditionally.

And conditional thinking is harder to sell.

A distribution is simply the range of possible outcomes that can happen after you take the trade. Not just win or lose, but the whole shape of the result: how often it wins, how often it loses, how large the winners are, how large the losers are, how ugly the path becomes, how much heat the trade takes, how stable the results are across time, and how sensitive the whole thing is to regime.

That distribution isn’t fixed just because the chart pattern has the same name.

The same entry signal on the same stock can produce one distribution in 2020 through 2023 and a completely different distribution in 2024 or 2025. The win rate may not even be the main issue. The average winner may shrink, the average loser may expand, the path may become more unstable. The move may still happen but no longer pay enough relative to the risk. The signal may still be visible, but the trade may no longer be tradable.

The setup didn’t necessarily disappear.

The distribution changed.

Once the distribution changes, the trade is no longer the same trade.

This is why “does this setup work?” is usually the wrong question. It sounds practical, but it hides the only part that matters.

The better question is:

Under what conditions does this action produce a stable, positive expectancy distribution?

A setup isn’t an edge. A setup is a trigger inside a state. The state determines the distribution. The distribution determines the expectancy.

The pattern isn’t the thing you trade.

The pattern is the visible clue inside a market condition you’ve already decided may be worth trading.

Where expected value lives

Conditional thinking only matters if you can evaluate whether the action is actually worth taking. That’s the job of expected value.

Expected value, often shortened to EV, is the average result you’d expect from taking a particular action over repeated attempts. In trading language, this is what people usually mean when they talk about edge.

Positive expected value means repeated interaction should tend to accumulate wealth, assuming you can survive the variance and size the bets properly. Negative expected value means repeated interaction should tend to destroy wealth, even if you occasionally get paid along the way.

The “assuming you can survive” part matters more than traders want to admit.

A strategy can have an attractive average outcome and still be unusable if the path is too violent, the drawdowns are too deep, or the sizing is reckless enough to kill you before the edge has time to show up.

Markets don’t pay you in averages. They pay you trade by trade, in sequence, with the size you actually used. If the path knocks you out before convergence, you never get to see the average.

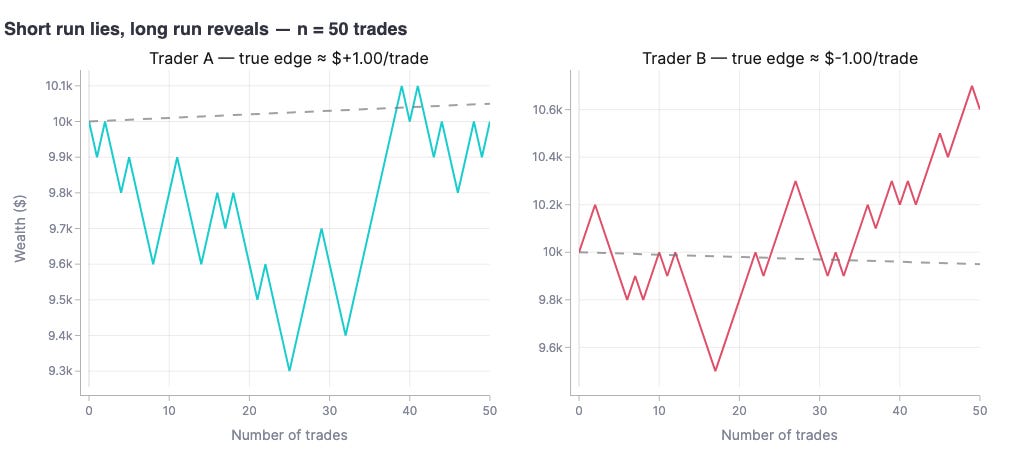

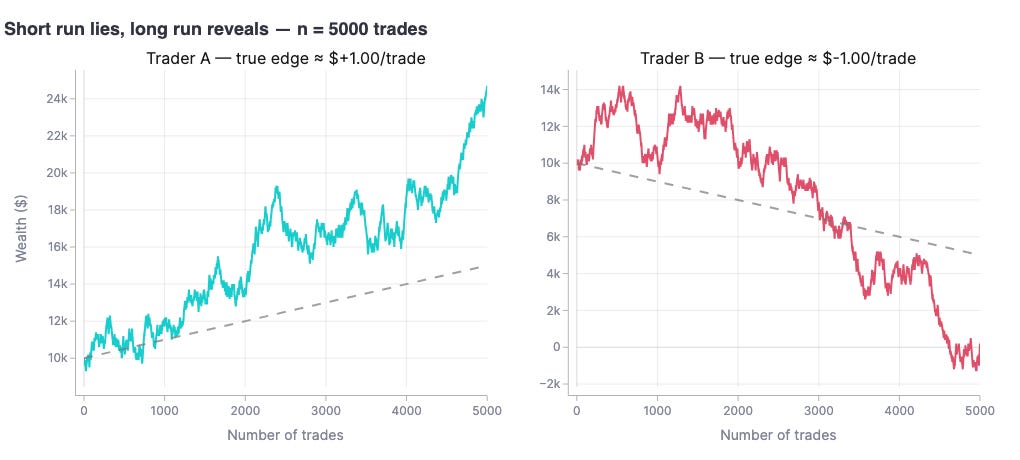

Markets are non-ergodic. The average outcome across a thousand parallel traders running the same strategy isn't the same thing as the path a single trader actually lives through. You don't get to be the average. You get to be one path. A strategy with positive expected value across a thousand simulations can still ruin the trader who hits the bad stretch first and can't pay rent. That's the entire reason sizing exists as a separate problem from edge.

This is why, when I review trades, the outcome of one trade is never the point.

Almost anything can win once. A bad setup, a chase, a revenge trade, a stop violation. A trade taken for no better reason than boredom can still print money.

That doesn’t make it good.

The question is what your actions are expected to produce over many repetitions, after uncertainty has had enough chances to express itself.

Most traders I see learn backward. They take a trade, observe the result, and then use the result to decide whether the setup worked. Green means good. Red means bad. Money came in, so the decision was right. Money went out, so the decision was wrong.

That isn’t learning. It’s outcome worship.

The trade result is information, but it isn’t a clean grade. A profitable trade may be evidence of good process, or it may be the market paying you to do something stupid. A losing trade may be evidence of a bad decision, or it may be the cost of a good decision operating in a probabilistic environment.

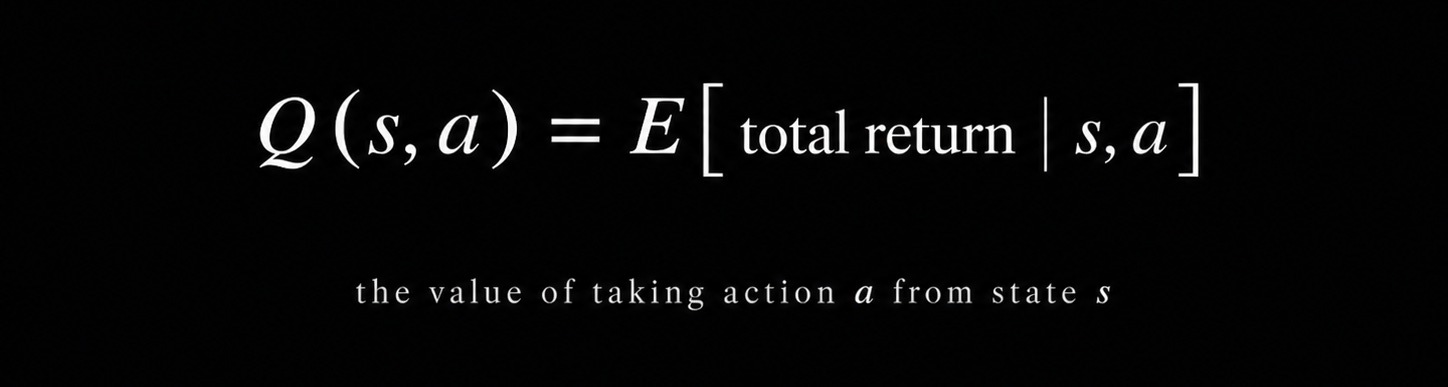

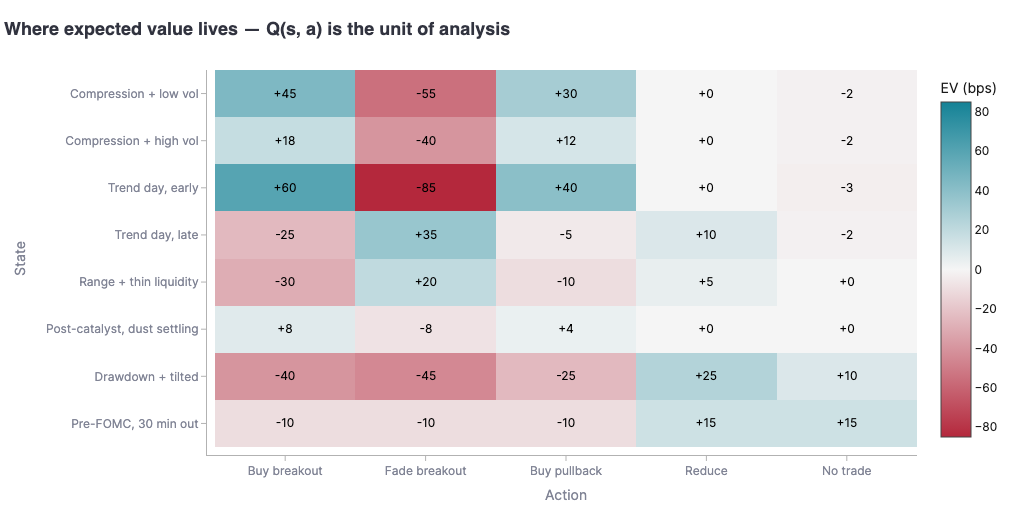

Once you understand expected value, the next mistake is placing it in the wrong object. Traders talk as if edge lives in the pattern, but it doesn’t.

Expected value lives in the state-action pair.

This is the distinction I wish more traders understood earlier.

“Breakouts work” is too crude a frame.

The real question is whether buying this breakout, in this state, with this size, at this location, against this liquidity, after this prior move, with this invalidation and this opportunity cost, has positive expectancy.

Reinforcement learning calls this Q(s, a). It just means: what’s the value of taking this action in this state.

Not the value of the pattern.

The value of the action from the state.

A pattern by itself doesn’t have stable meaning. A breakout can be continuation in one state, exhaustion in another, noise in a third. In a fourth, it’s a gift to people who were already long and needed liquidity to exit.

This is why the question “does this setup work?” can trap traders for years. It sounds like the right question, but it hides the state.

The better question is: in which states does this action have positive expectancy, and under what constraints does that expectancy survive?

A trade can have positive expected value in theory and still be a bad action in practice if the size is wrong, the cost is too high, the liquidity is too thin, the tail risk is too ugly, or the trade consumes risk budget needed for something better.

Professional trading isn’t trying to maximize raw profit on one decision. It’s trying to maximize expected utility over time after risk, cost, drawdown, liquidity, constraints, and future opportunity are included.

That sounds academic until you’ve watched a “winning trade” wreck the rest of someone’s week.

Then it stops sounding academic.

At 5,000 the edge is undeniable. The realized line vs the dashed theoretical line is the difference between what a trader thinks is happening and what's actually true.

Illustrative only. “Buy breakout” can have +60 bps of edge in one state and −25 bps in another. Same state has multiple positive-EV actions, or zero, depending on what's going on around it. Edge isn't in the pattern. It's in the state-action pair.Markets are not roulette

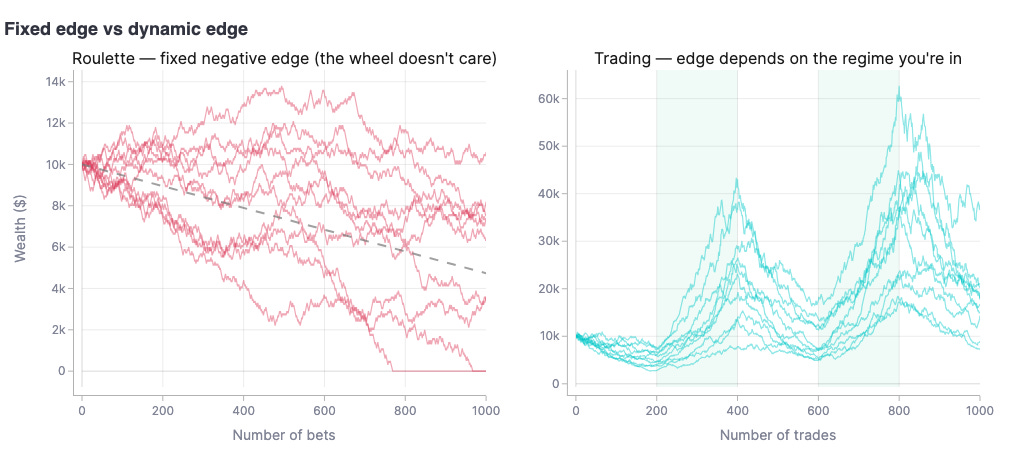

EV by itself isn’t enough, because the edge in trading doesn’t sit still the way it does in a casino game.

Roulette is useful because it shows what markets aren’t. The rules don’t change, the wheel doesn’t adapt to you, the probabilities are stable, the outcomes are known, the edge is fixed. If you bet on black you might win the next spin, but over time the payout structure creates negative expected value for the player and positive expected value for the casino.

The casino wants volume. It doesn’t care who wins the next spin, just that another one is coming with the same edge baked in.

The player can have a lucky night, double his money, and walk away convinced he has a feel for the wheel. But if he keeps playing a negative expected value game for long enough, the math grinds him down.

That’s a fixed-edge environment.

Trading isn’t that.

In trading, edge is dynamic. The probability of an action working isn’t fixed across time, regime, liquidity, positioning, volatility, catalyst structure, or participant behavior. The same action can have positive expected value in one state and negative expected value in another. The same setup can work beautifully for months, then stop working right when the trader has the most confidence in it.

Fixed system education has to avoid this part because the messier truth doesn’t package as well.

A fixed rule set is clean. A dynamic edge is messy.

“Buy this breakout pattern when these criteria appear” is easier to package than “learn to identify the states where buying this breakout has positive expected value, then adjust the action for volatility, liquidity, risk, cost, account state, and future opportunity.”

The second version is uglier.

It’s also closer to the truth.

Blackjack gets us closer than roulette because now policy starts to matter. If you hit or stand randomly, your expected value is terrible.

If you follow a better basic strategy, your expected value improves. If you count cards well, understand the state of the deck, and adjust bet size properly, you can change the game enough that the expected value becomes favorable under the right conditions.

The important part isn’t blackjack itself. The important part is the mechanism: your action policy influences your expected value.

There’s a subtle trap here.

A better policy isn’t the same thing as a positive expected value policy. A blackjack player can choose a better rule and still be playing a losing game. He can lose slower, lose cleaner, lose with more discipline, and still lose.

Trading has the same trap.

A trader can improve a bad setup, add filters, avoid the worst entries, stop chasing dead midday breakouts, and still not have a process worth risking capital on.

Better than before isn’t the same as good.

Poker gets closer still because now you have incomplete information, adaptive opponents, hidden state, bet sizing, position, table dynamics, and psychology. The cards matter, but the cards aren’t the whole decision.

Pocket aces are the strongest starting hand in poker, but even aces do not make the decision for you forever.

Preflop, they are usually worth playing aggressively. But once the hand develops, the state changes. Board texture, position, stack depth, bet sizing, opponent range, and the story being told can all turn a once-dominant hand into a difficult decision.

The strength of the hand is one input. The decision is the action you choose from the full state.

Trading is closer to poker than roulette, but with more moving parts. The game is partially observable, the participants adapt, costs matter, liquidity changes, regimes shift, volatility expands and contracts. Leverage can kill you. The same thing that worked yesterday can decay without warning.

You aren’t playing a fixed wheel.

You’re operating inside a live environment where your edge depends on the state and the action you choose from it.

ten people grinding on roulette. The wheel pays the casino a fixed cut on every spin. The math just runs. Right: ten traders in a market where the edge flips between favorable (shaded) and unfavorable. A trader who can't read the regime is forced to take both. The casino doesn't care if you can read state. The market does. So that’s the diagnosis as I see it.

Setups are not edges.

Edges depend on state. State changes. Feedback is noisy. A good decision can lose. A bad decision can get paid. And the pattern can survive long after the condition that made it work has quietly disappeared.

That is how traders get trapped.

They keep clicking the same familiar chart pattern while the distribution underneath it has changed.

Fine.

The harder question is what replaces it.

If the system isn’t the job, what is? If a setup is only a trigger inside a state, what does the actual decision process look like? How do you size? When do you sit out? What does discretion really mean? And how do you keep the market from teaching you the wrong lesson while it is paying you?

That’s Part 2:

And if you want the full framework, my book, The Art & Business of Professional Trading, is now out from Wiley.

As a developing trader who’s found profitably in the past 5 weeks, hands down, this is your best article to date. I totally know what you mean about state - in fact, I wished I learnt this 3 years ago! So much time and energy to learn a simple (yet complex) concept

For anyone curious, Ryan's book is similar in depth and insights to this article. I'm 80% through with it and it's one of the best books on the subject. Nothing really like it out there.